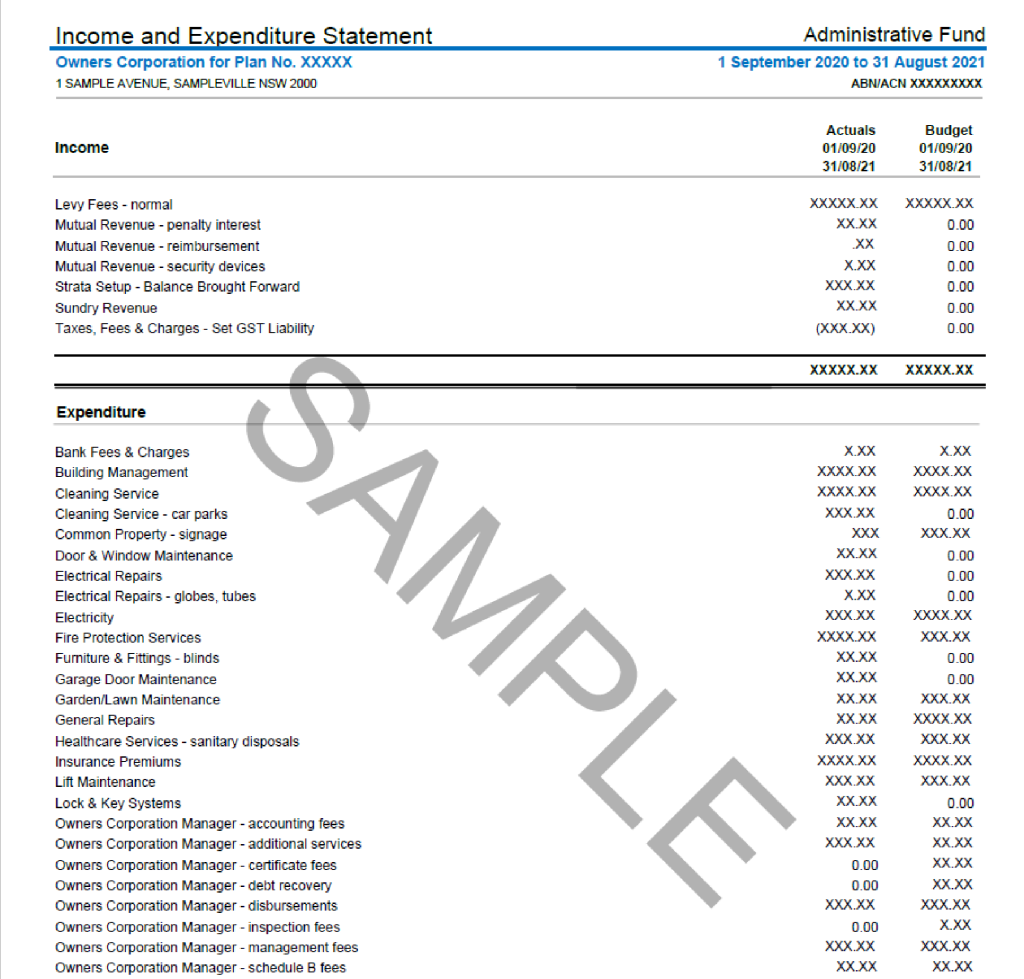

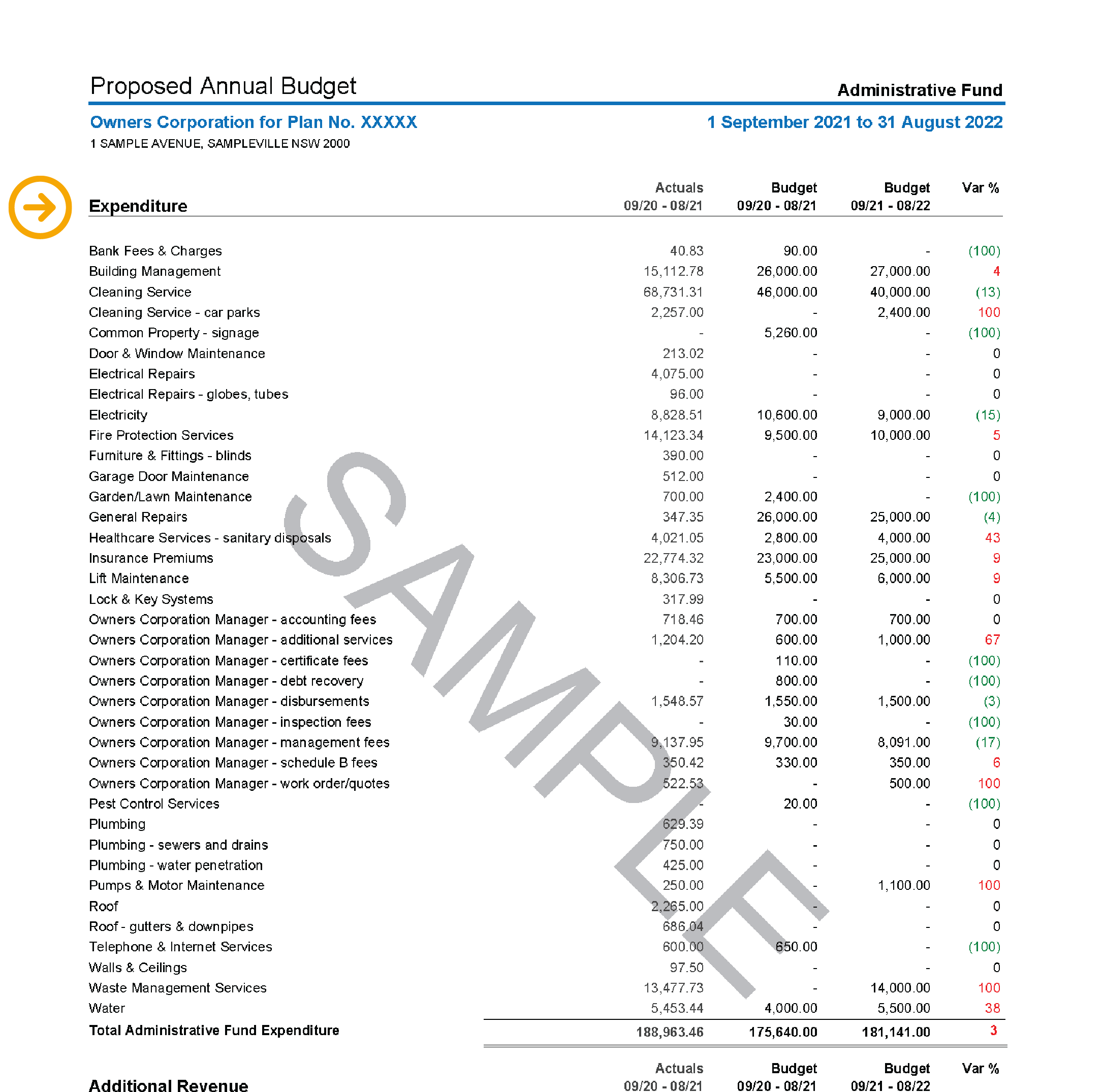

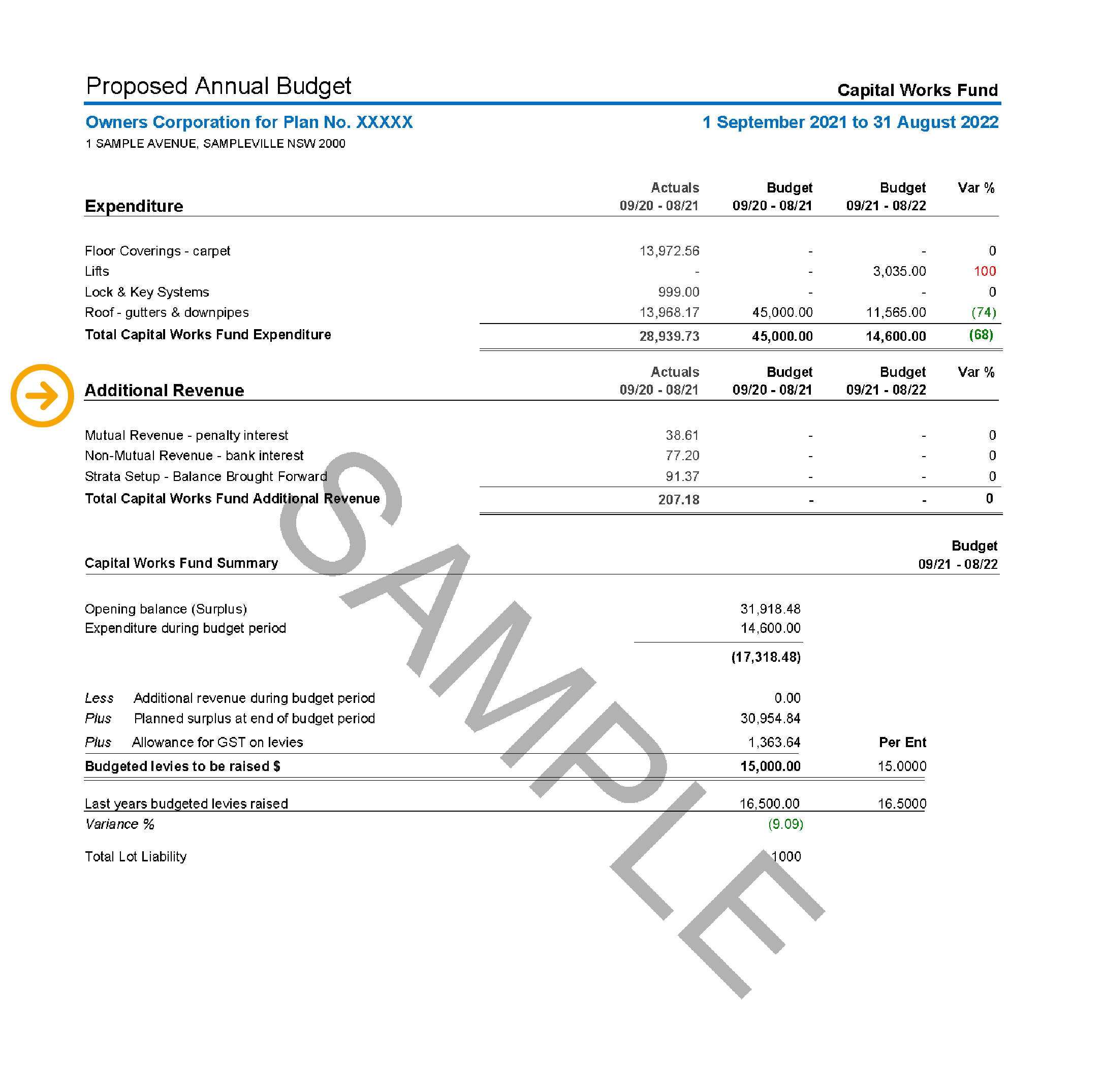

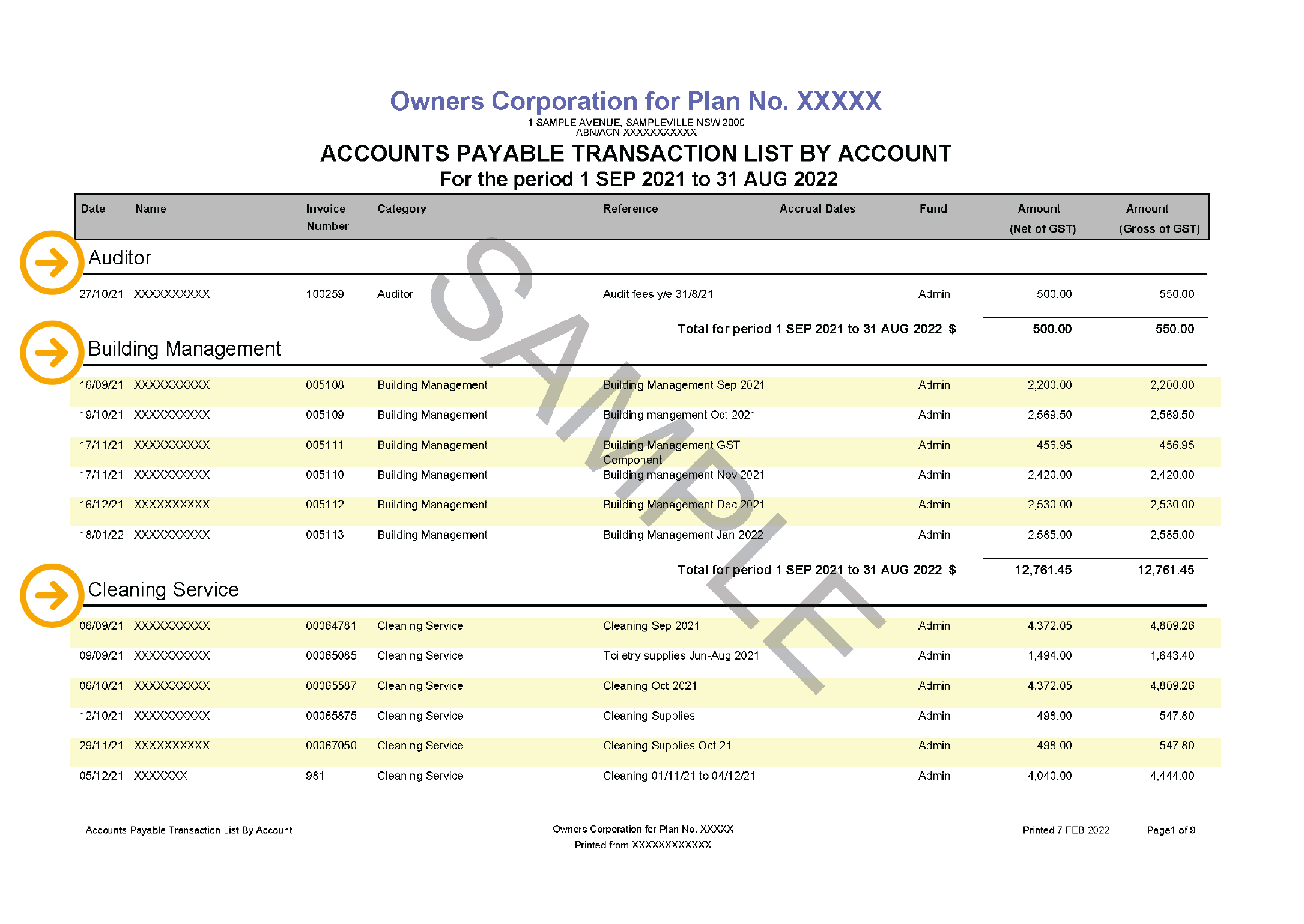

This section breaks down all reasonably expected costs for the financial year ahead within account codes. These are used to group similar expenses, such as general repairs or lawn maintenance. The budgeted amount for each line item is based on the previous year’s spending, as shown in this report.

This section includes any revenue the property may receive, not including levies issued to owners. Additional revenue includes bank interest on deposits, penalty interest on late payments, recoveries from owners for costs incurred (e.g., debt recovery), leases or licence fees.

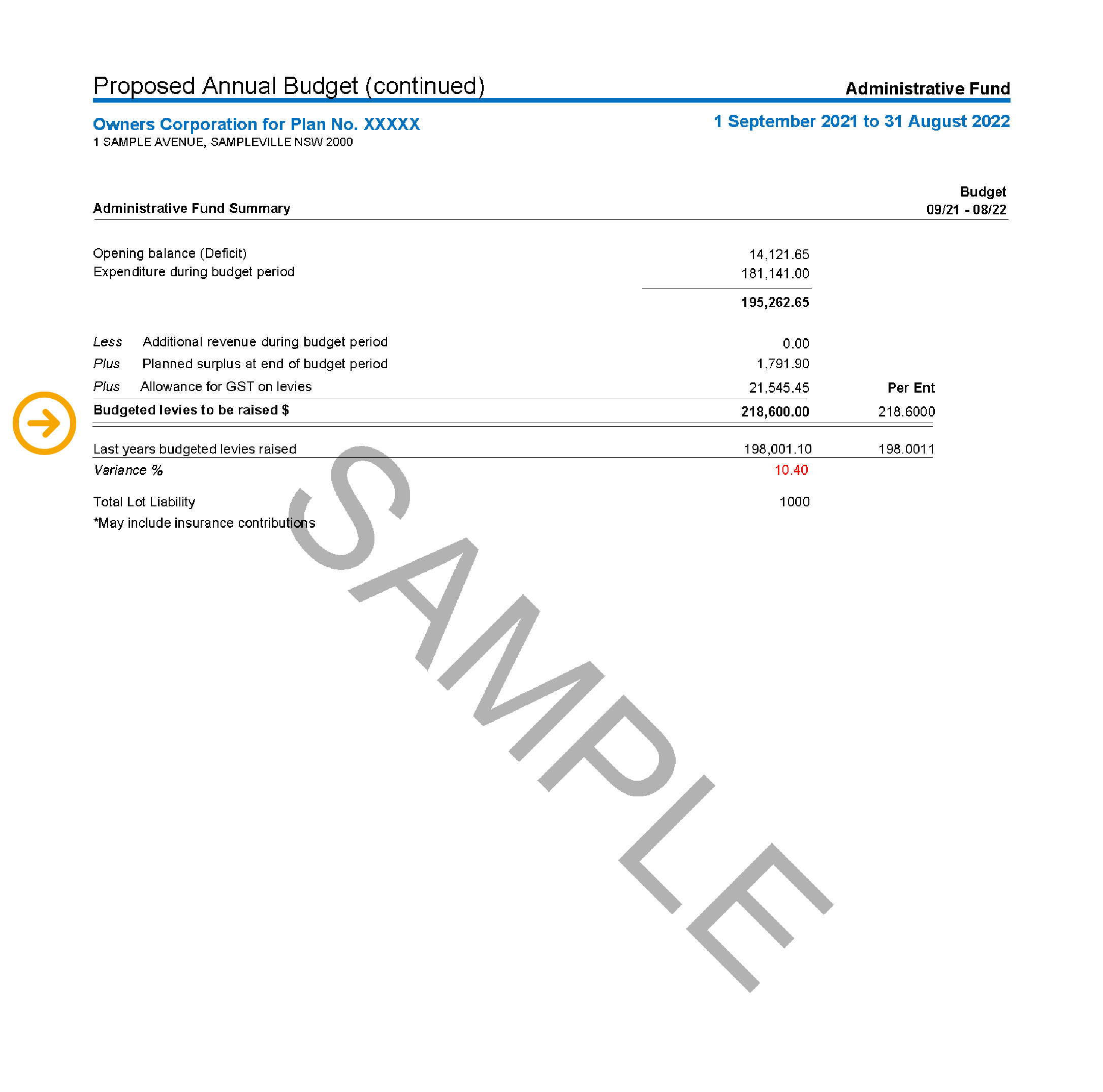

The levies proposed within the budget will be the amount the owners are required to contribute to cover the owners corporation or body corporate expenses. Sometimes, where a contracted or guaranteed additional revenue stream is available, this fund may be used to reduce the amount required to be raised from owners.

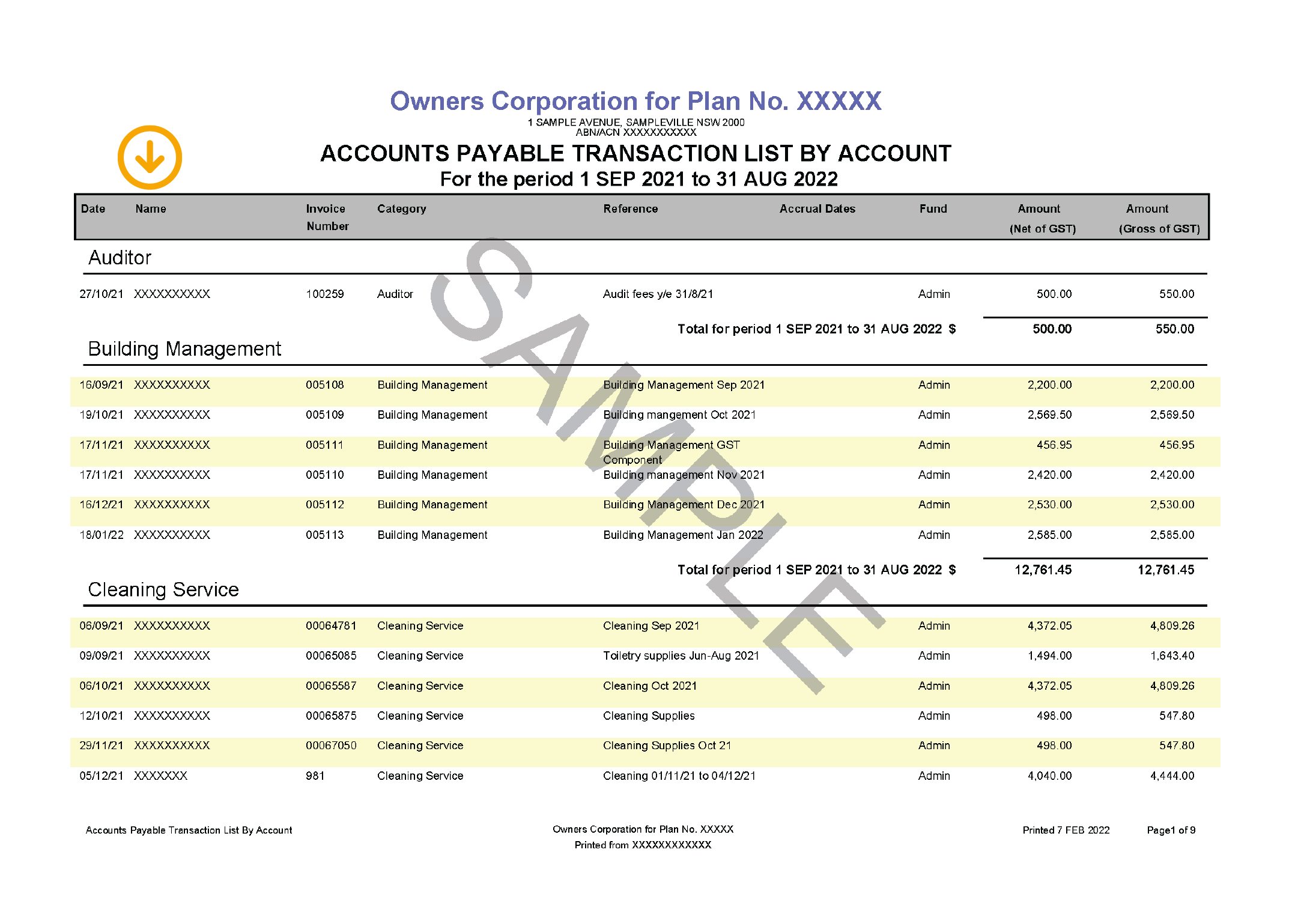

Name of the supplier, business or contractor the owners corporation or body corporate has paid.

This section outlines the category of service the supplier provides, such as cleaning or gardening.

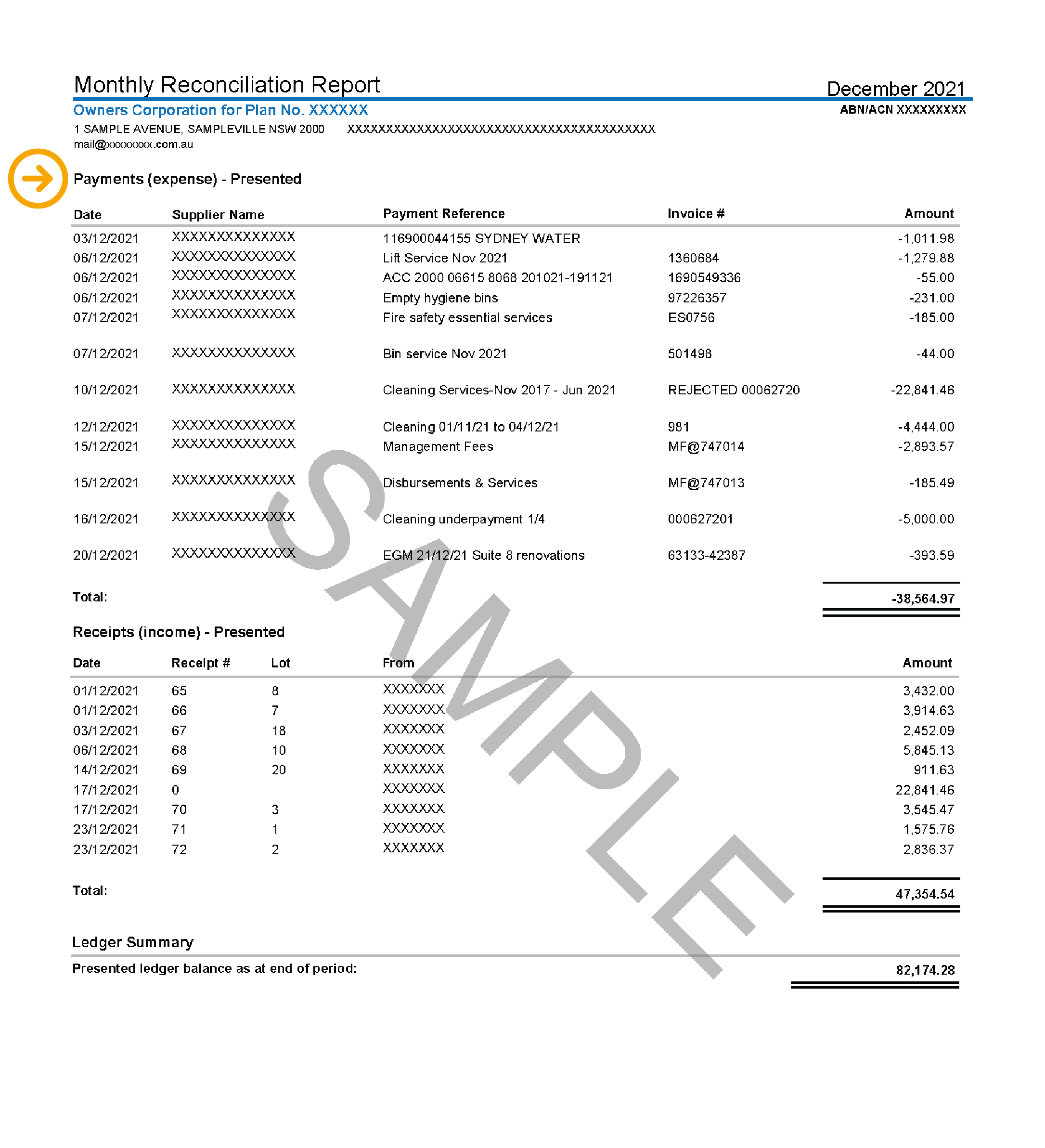

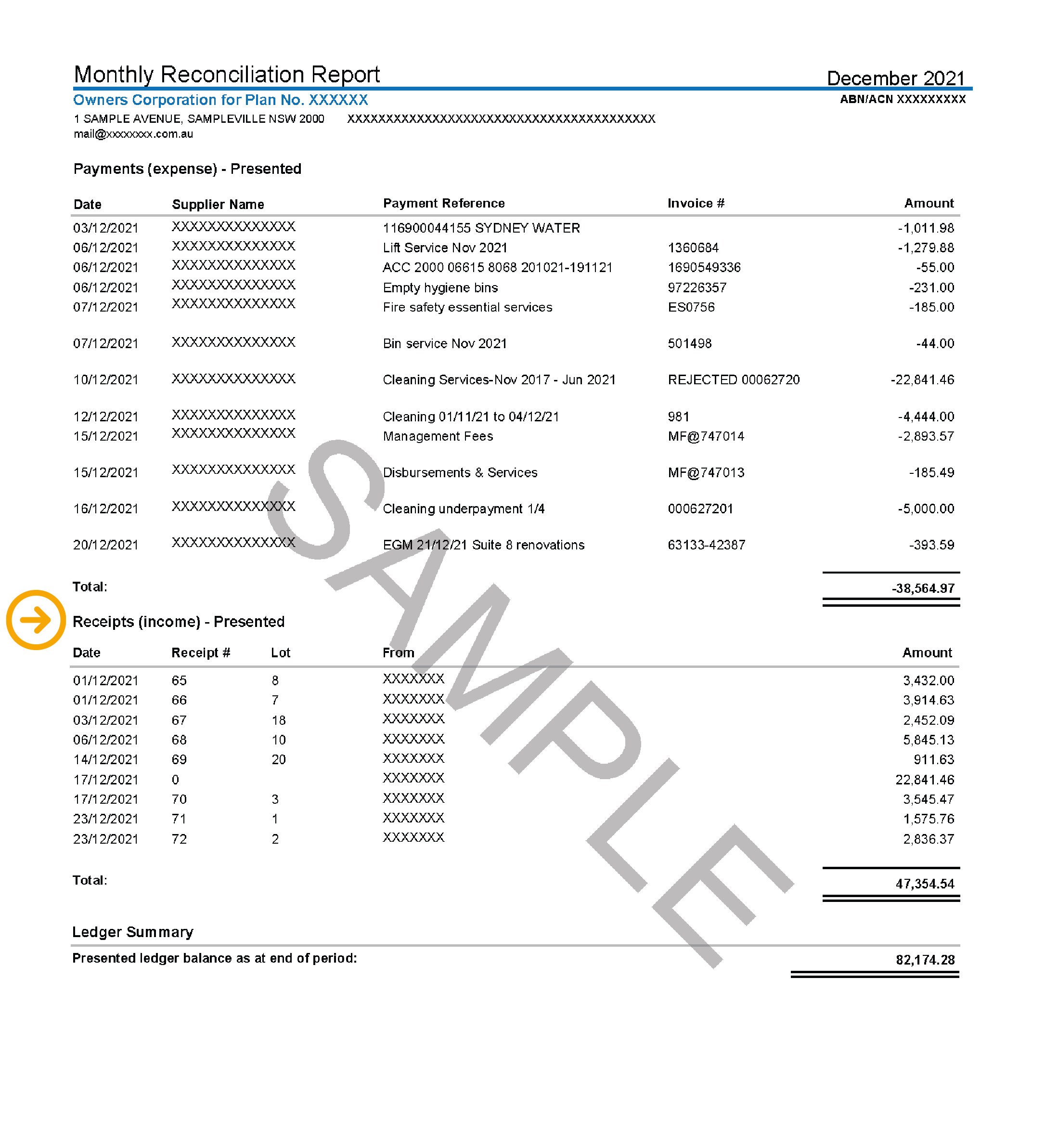

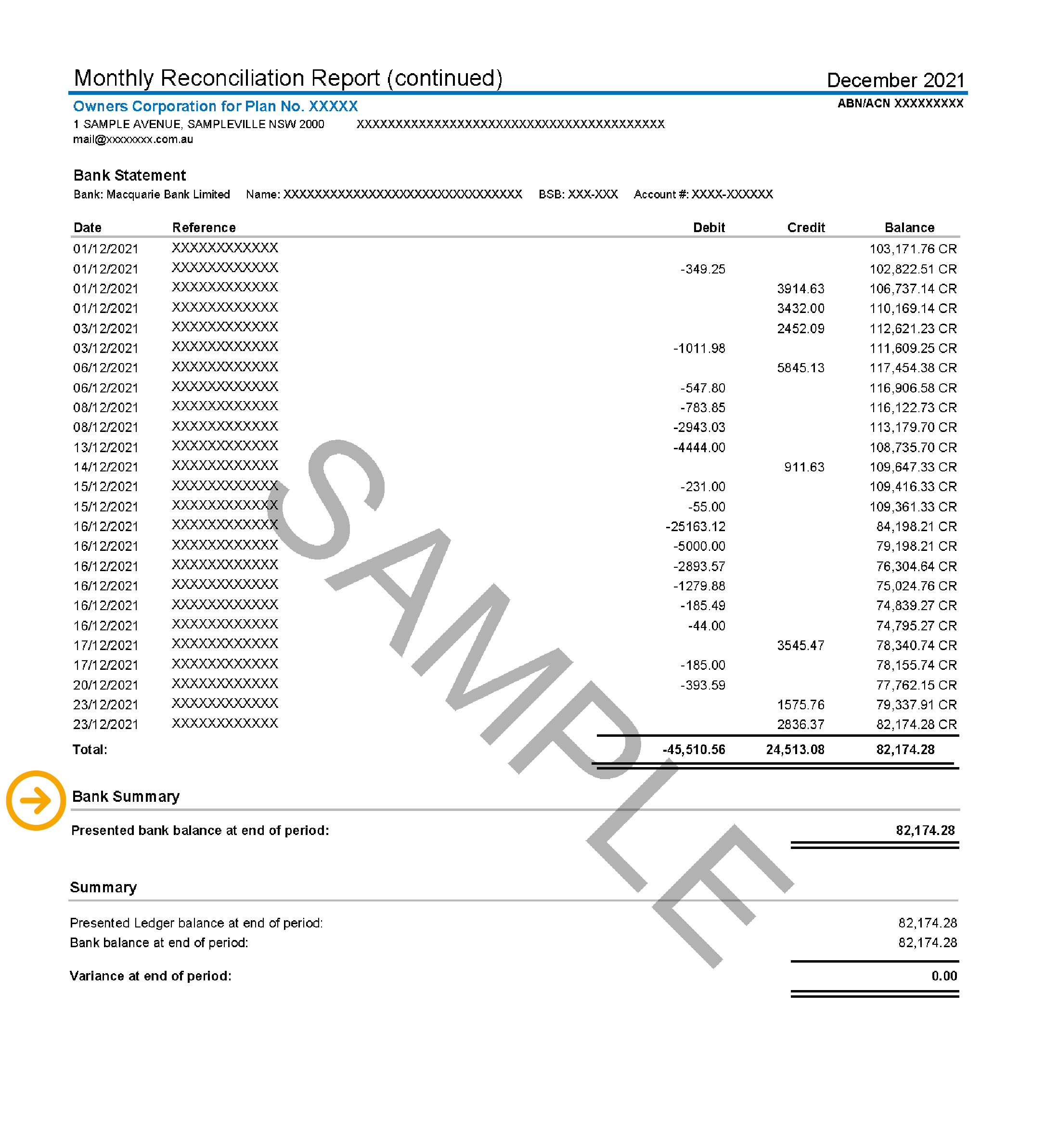

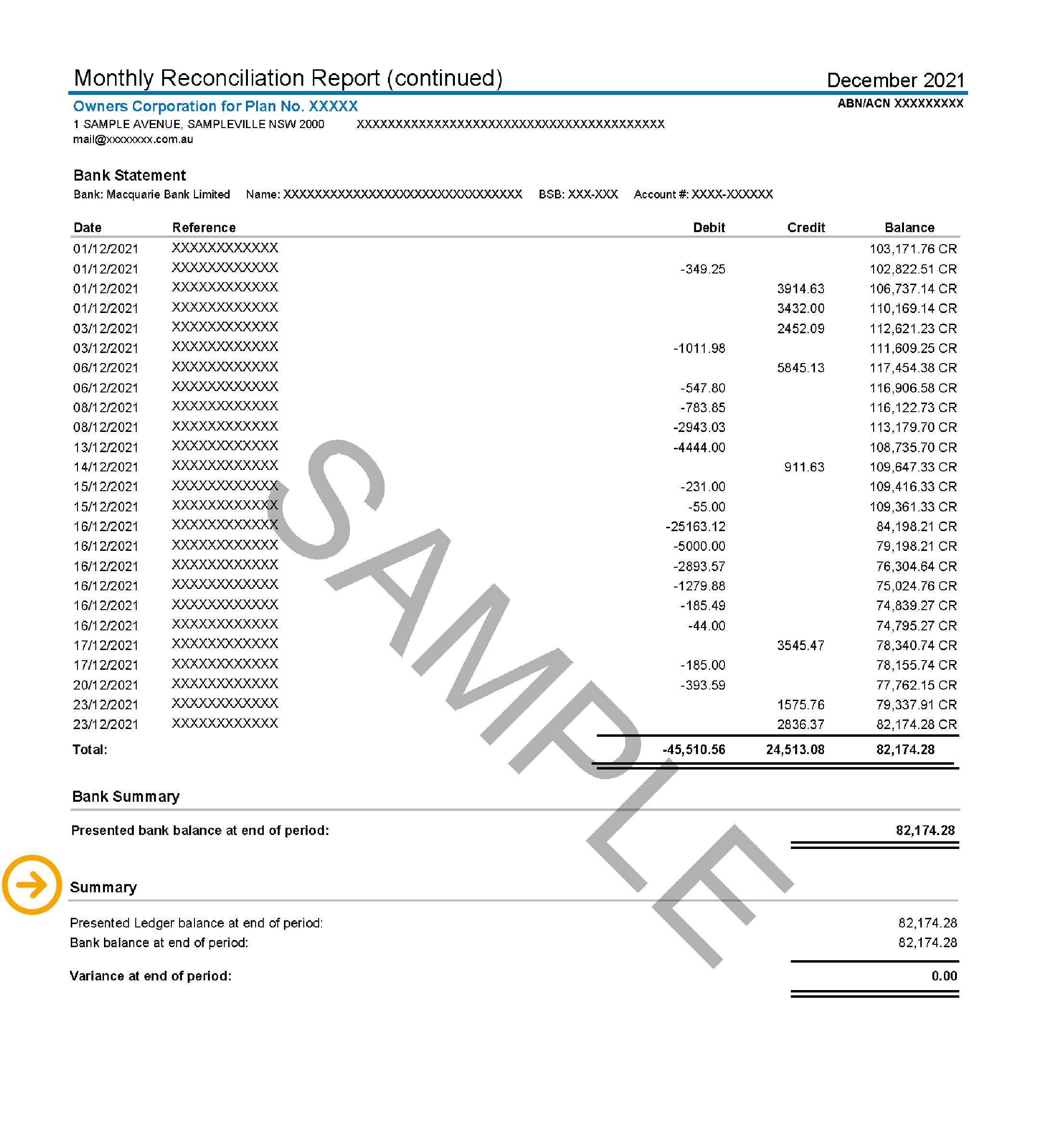

All payments made during the month, such as supplier payments.

Identifies the source of income, such as levy payments. In this section levy payments will include the lot number and amount.

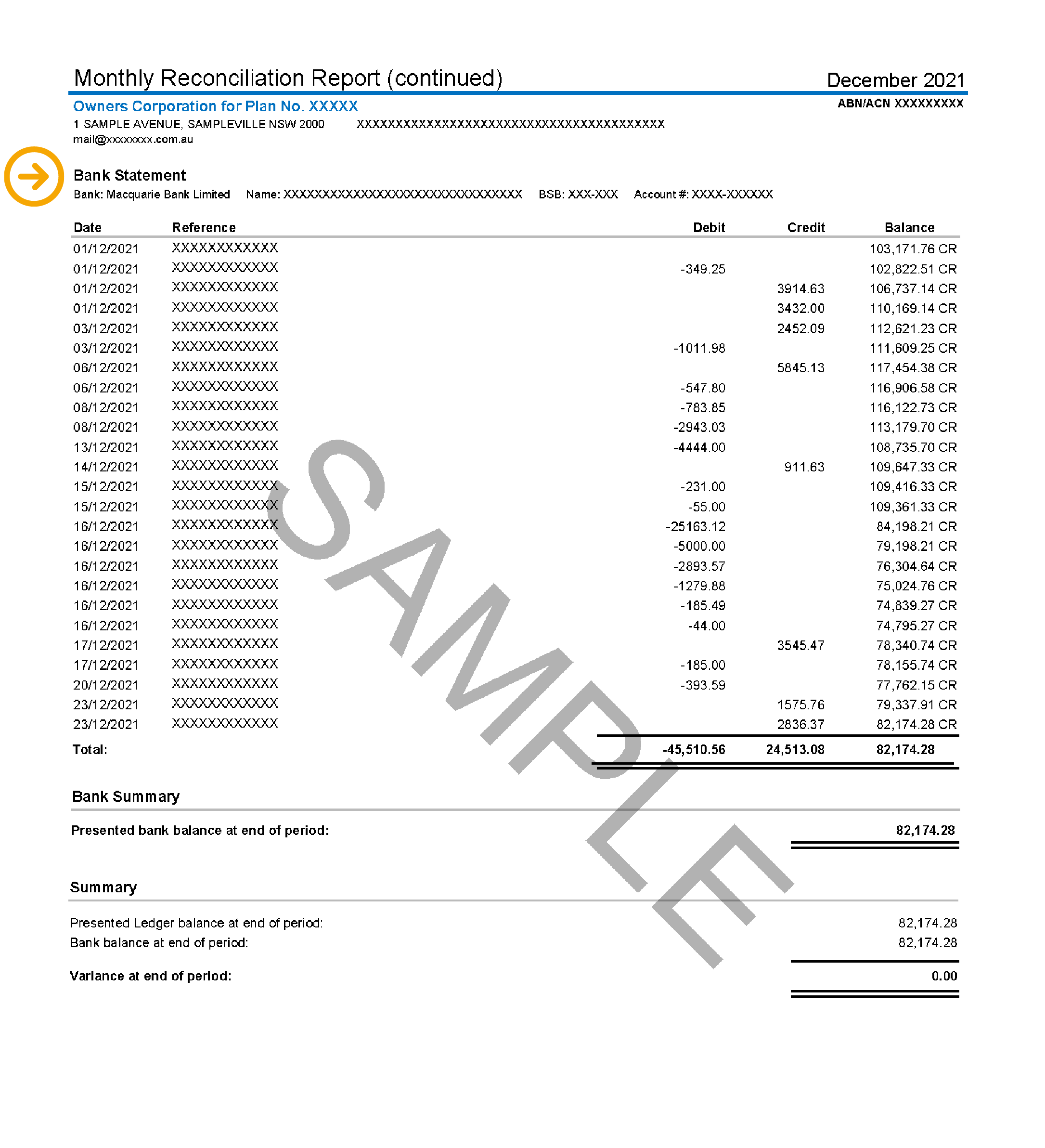

View each transaction (debits or outgoings and credits or incoming) in order, along with the original references.

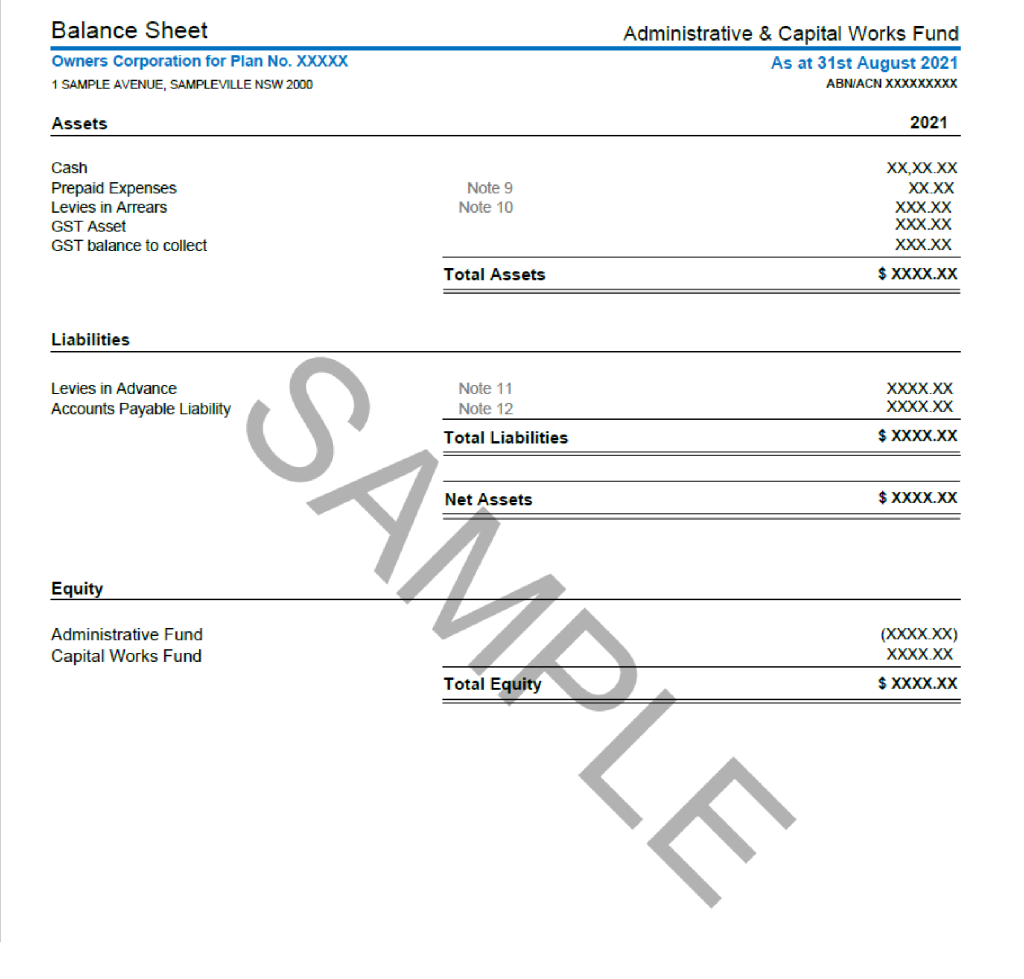

Cash in bank figure at the end of the period.

Details the presented ledger balance and the bank balance at the end of the period. Any variance will be shown.

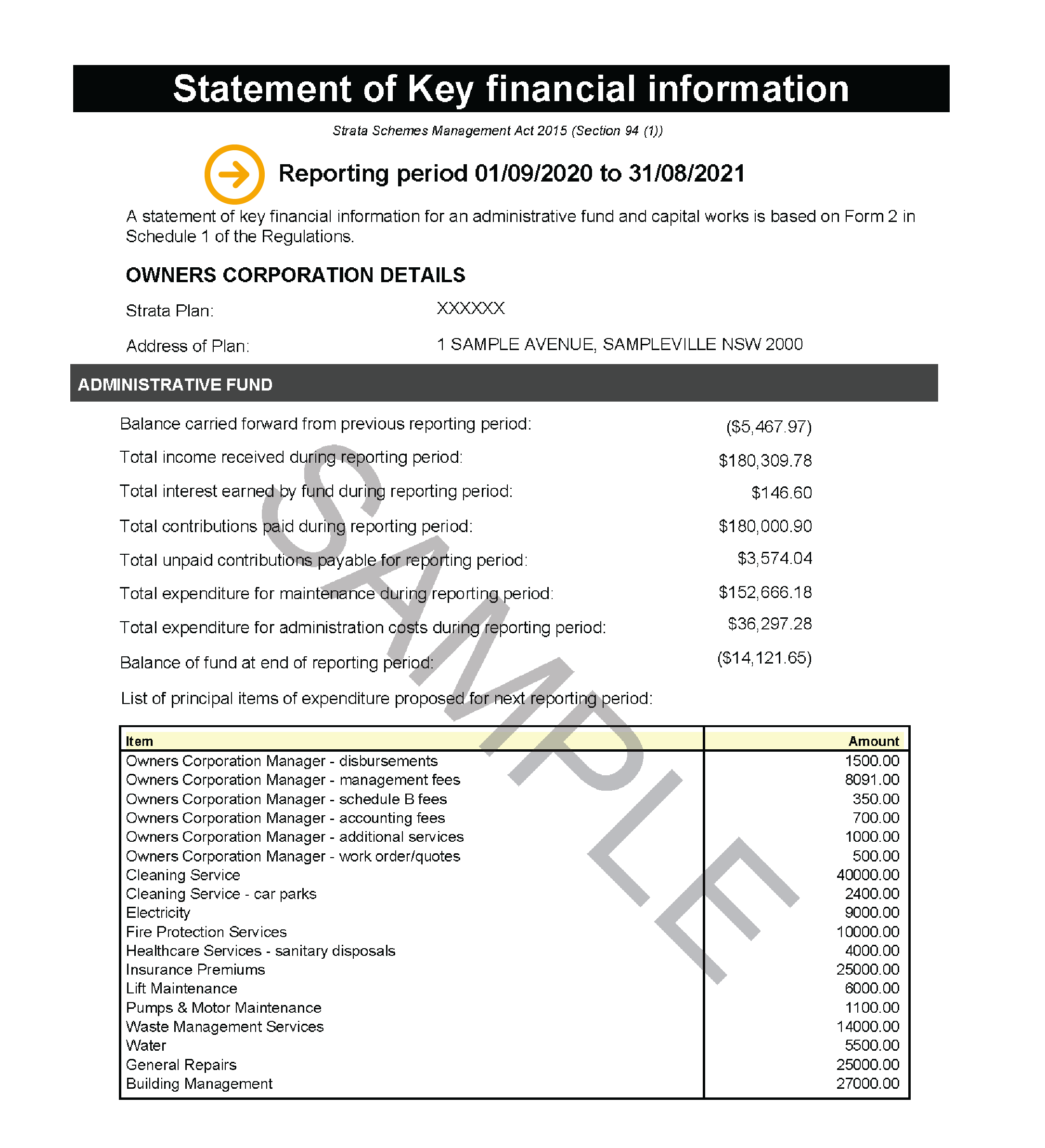

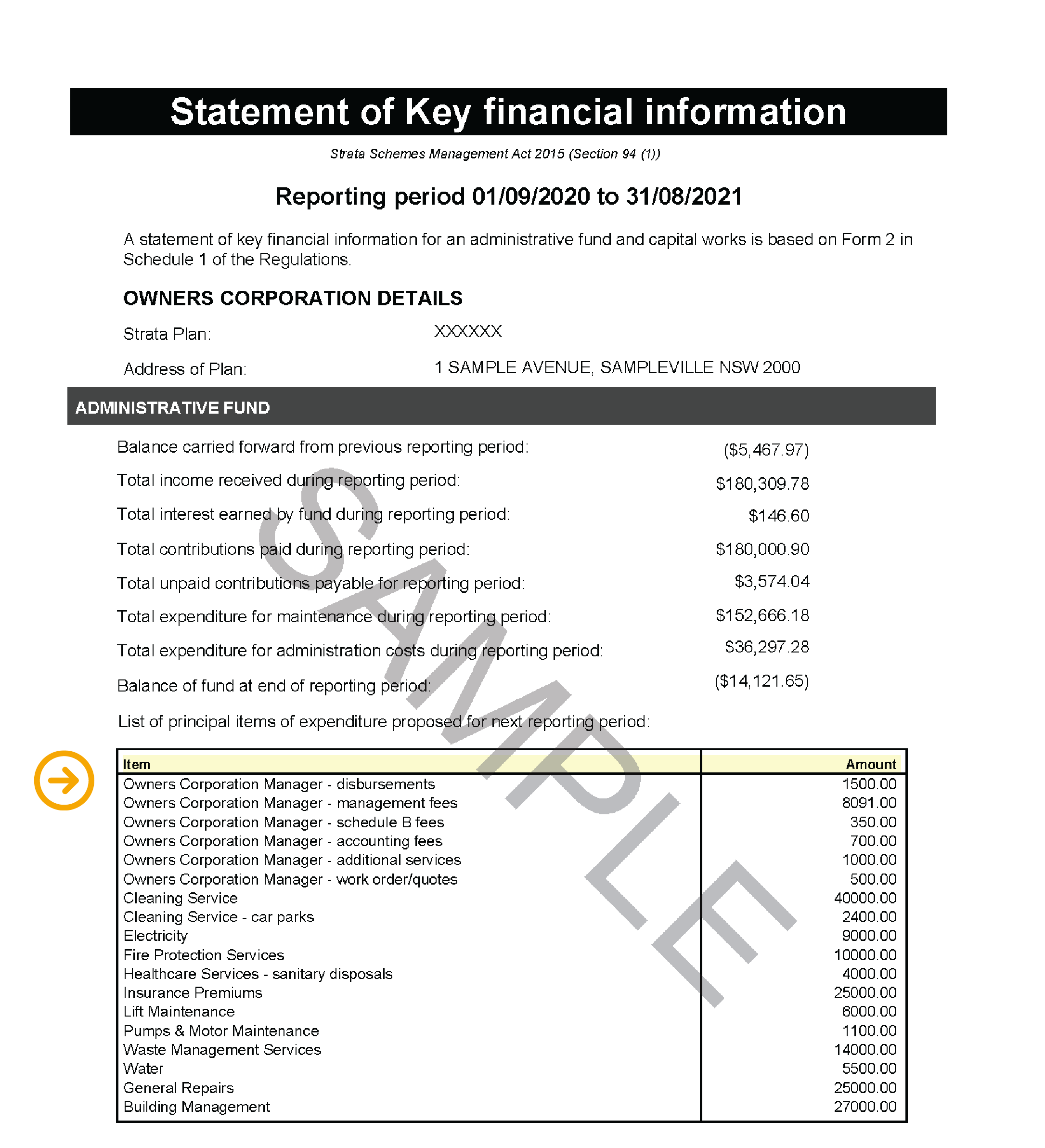

This section outlines the time period that this financial report covers.

This overview provides a high-level summary of the administrative fund’s income and expenditure during the reporting period.

An itemised summary of all of the administration fund’s expenses during the reporting period.

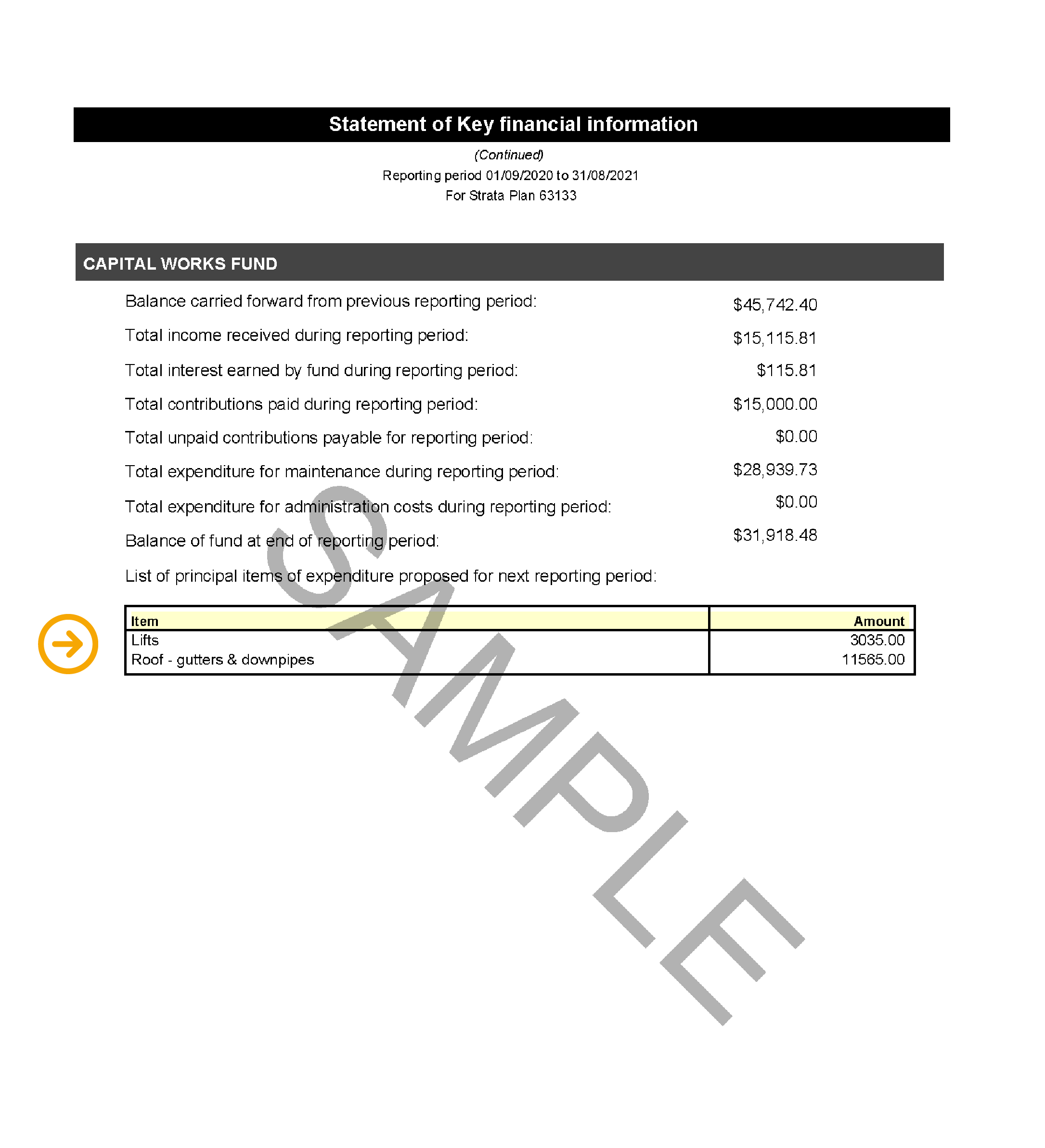

Provides a high-level summary of the capital works or sinking fund income and expenditure during the reporting period.

An itemised summary of all of the capital works/sinking fund expenses during the reporting period. View report layout

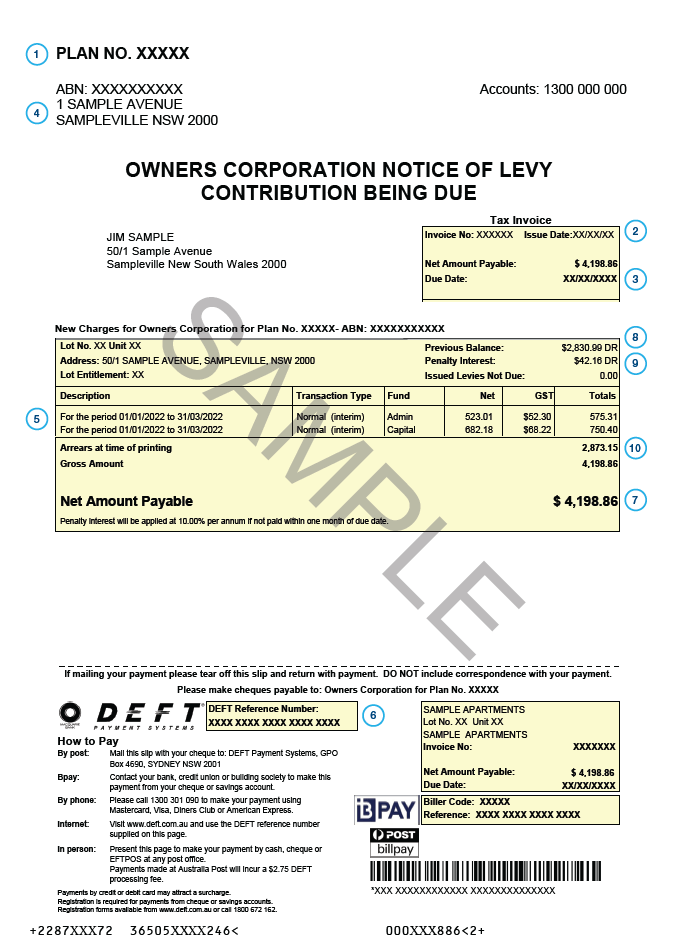

Plan number

Issue date

Due date

Strata scheme/body corporate/owners corporation address

Levy period

DEFT reference number

Total amount payable.

Previous balance – balance brought forward.

Penalty Interest.

Arrears at the time of printing = previous balance + penalty interest.