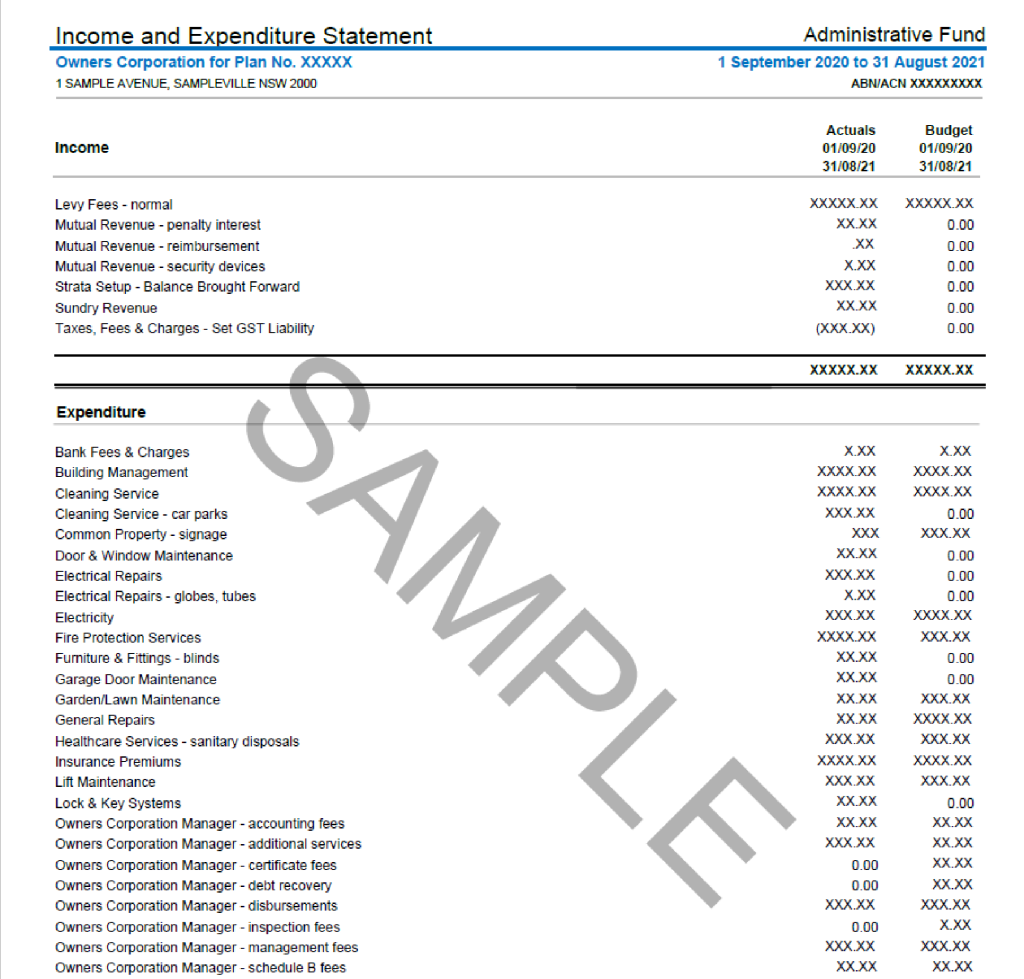

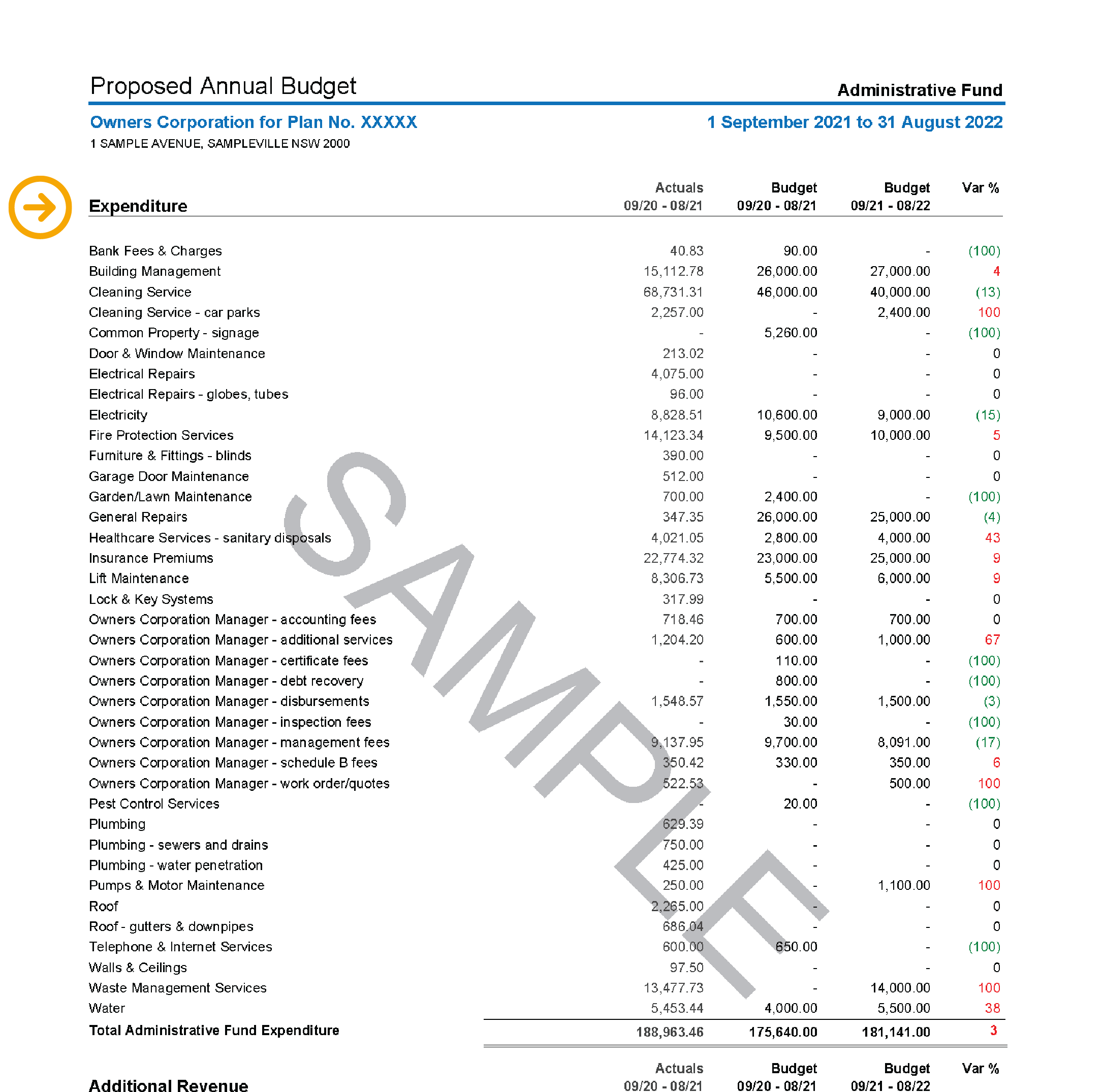

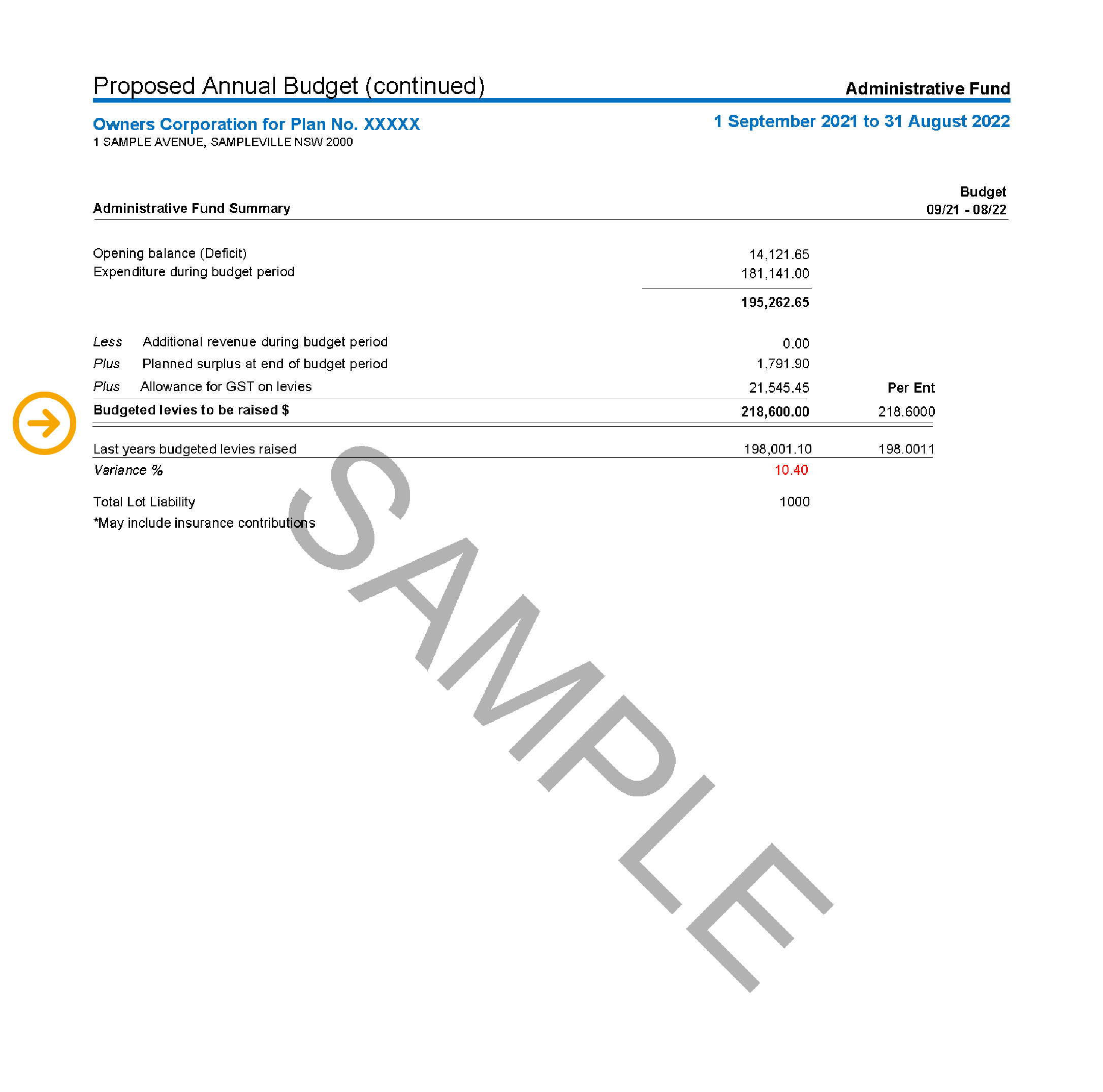

Administration fund

This fund holds money that is set aside for day-to-day recurrent operating costs for your property. It may include some maintenance items if they are regular, routine and recurrent, such as a lift maintenance contract and fire and essential services inspections.

Annual financial statements

These are prepared for your property’s 12-month financial year.

They include the balance sheet, income statement, notes to the financials, and key financial information statements.

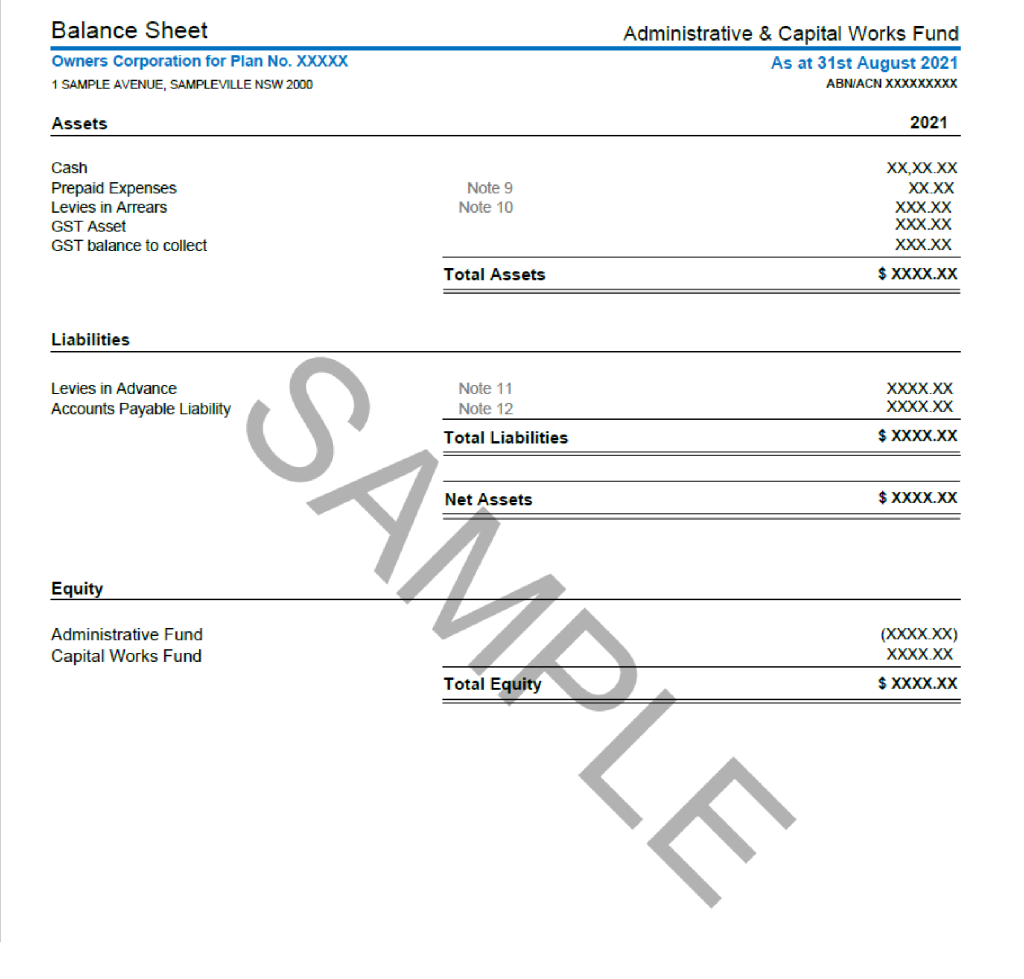

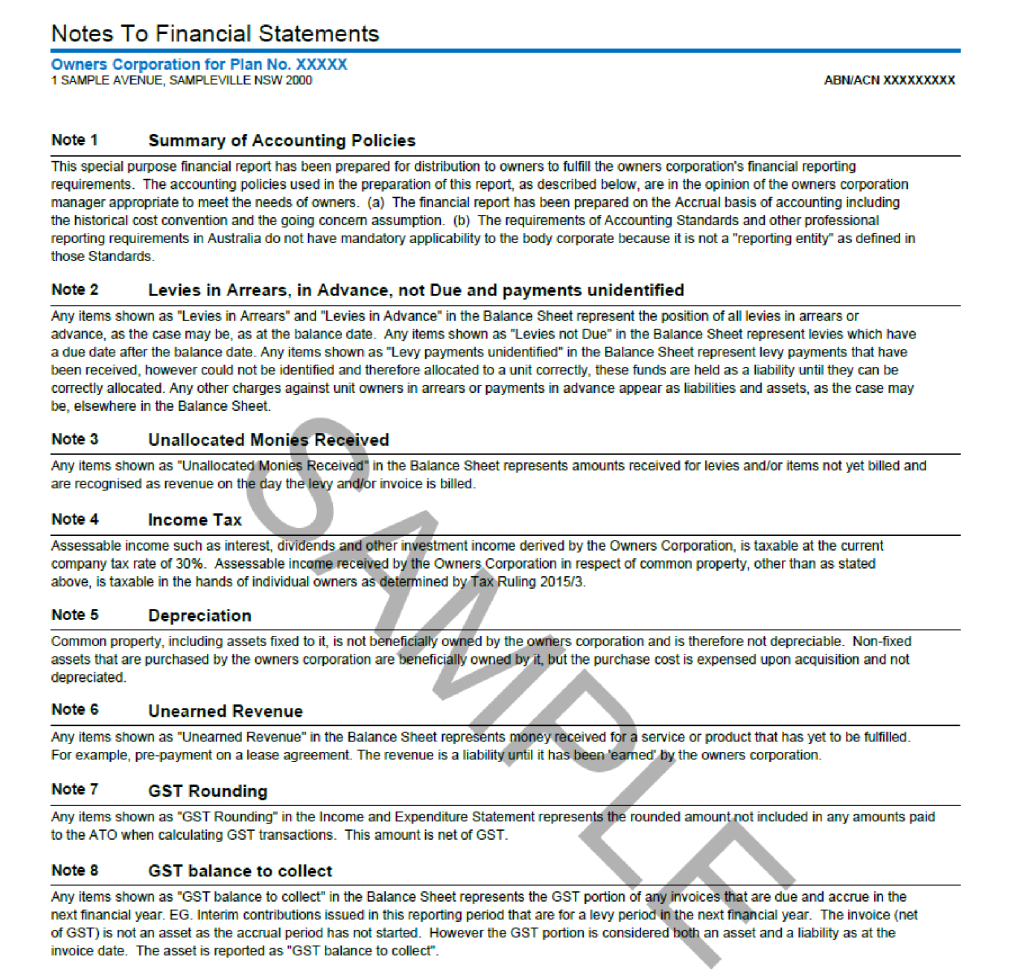

Assets

These items are owned by the owners corporation or body corporate, such as cash in the bank, money owed by lot owners for unpaid fees, or money due to be received from an insurance settlement. Generally, physical assets such as furniture, furnishings, buildings, and equipment are written off in the year they are purchased and do not depreciate over time. Therefore, they are not recorded as assets on the balance sheet.

Transaction of operating account – also known as an at call bank account

This is an account where the owners corporation or body corporate funds are stored to allow payment of expenses and receive levy payments from lot owners.

Balance sheet

This details what the owners corporation or body corporate owns (assets), what it owes (liabilities) and what lot owners are entitled to if the property is dissolved (equity).

Capital, equity, and members funds

If there is a positive balance when the liabilities are subtracted from the assets, this extra money is held in this fund. This surplus is what each lot owner is entitled to if the strata property is dissolved.

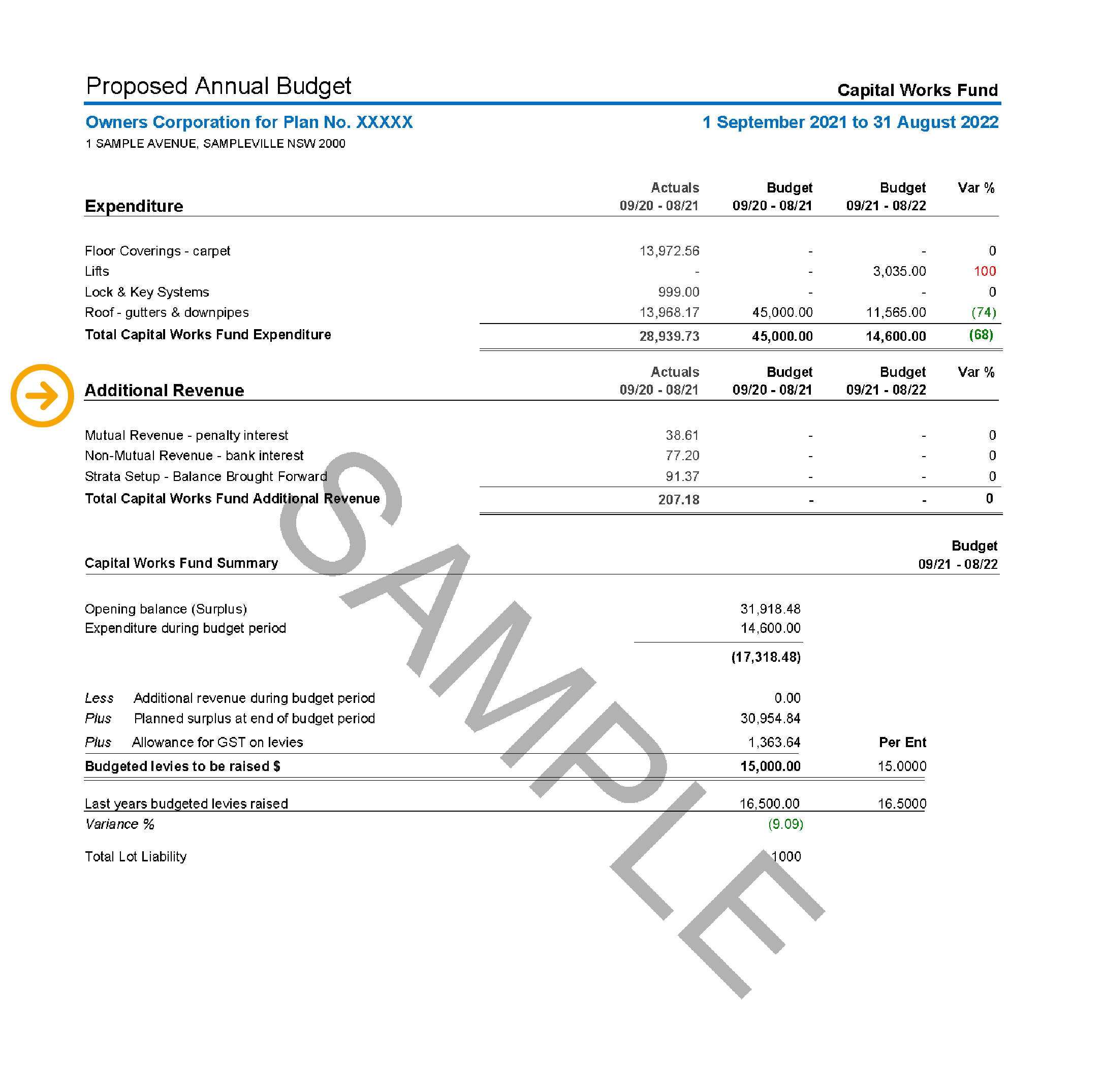

Capital works or sinking fund

A capital works, sinking, or maintenance fund is a pool of money the owners corporation or body corporate sets aside for the future maintenance of the property. All owners contribute to this fund with each levy paid.

Deficit

A deficit will occur when expenses paid are greater than income received. If there are recurring deficits, the strata levies will need to be increased or expenses reduced.

Expenses

These are costs incurred by the owners corporation or body corporate. Examples include insurance premiums, utility bills, council charges, compliance fees (fire safety, ventilation systems, access, etc.), caretaker or building manager fees, and strata management fees.

Financial year

This is not the Australian financial year from 1 July to 30 June. Your strata property’s financial year is the agreed annual period to which the owners corporation or body corporate prepares and manages finances. It may be different from property to property.

Income

This is the money the owners corporation or body corporate receives. It consists of strata levies paid by owners, interest accrued (either bank or penalty interest for late payment), reimbursed money, and lease or license income